ON CORPORATE FINANCE & MACROECONOMICS

Publications

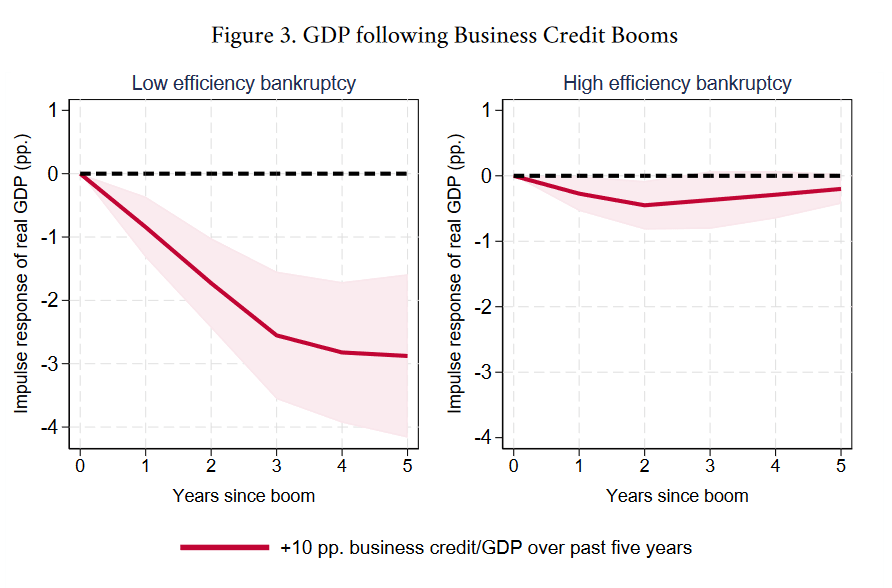

Bankruptcy Resolution and Credit Cycles

with Chen Lian, Yueran Ma, Pablo Ottonello and Diego Perez

We study how the macroeconomic implications of credit cycles vary with business bankruptcy institutions. Using data on bankruptcy efficiency and business credit across countries, we document that business credit booms are followed by severe declines in output, investment, and consumption in environments with poorly functioning business bankruptcy. On the contrary, in settings with well functioning business bankruptcy, the aftermath of credit booms is characterized by moderate changes in economic activities. We use a simple model to lay out how and when efficient bankruptcy systems can mitigate the negative consequences of credit booms.

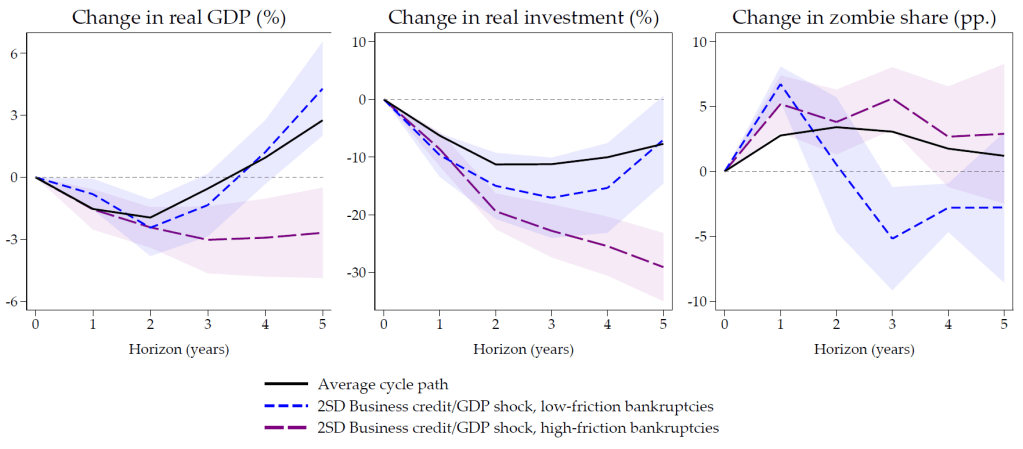

Zombies at Large? Corporate Debt Overhang and the Macroeconomy

with Òscar Jordà, Moritz Schularick and Alan Taylor

Debt overhang is associated with higher financial fragility and slower recovery from recession. However, while household credit booms have been extensively documented to have this property, we find that corporate debt does not fit the same pattern. Newly collected data on non-financial business liabilities for 18 advanced economies over the past 150 years shows that, in the aggregate, greater frictions in corporate debt resolution make for slower recoveries, with weak investment and more persistent „zombie firms“ and that this is an important factor in explaining the difference in outcomes relative to household credit booms.

Working Papers

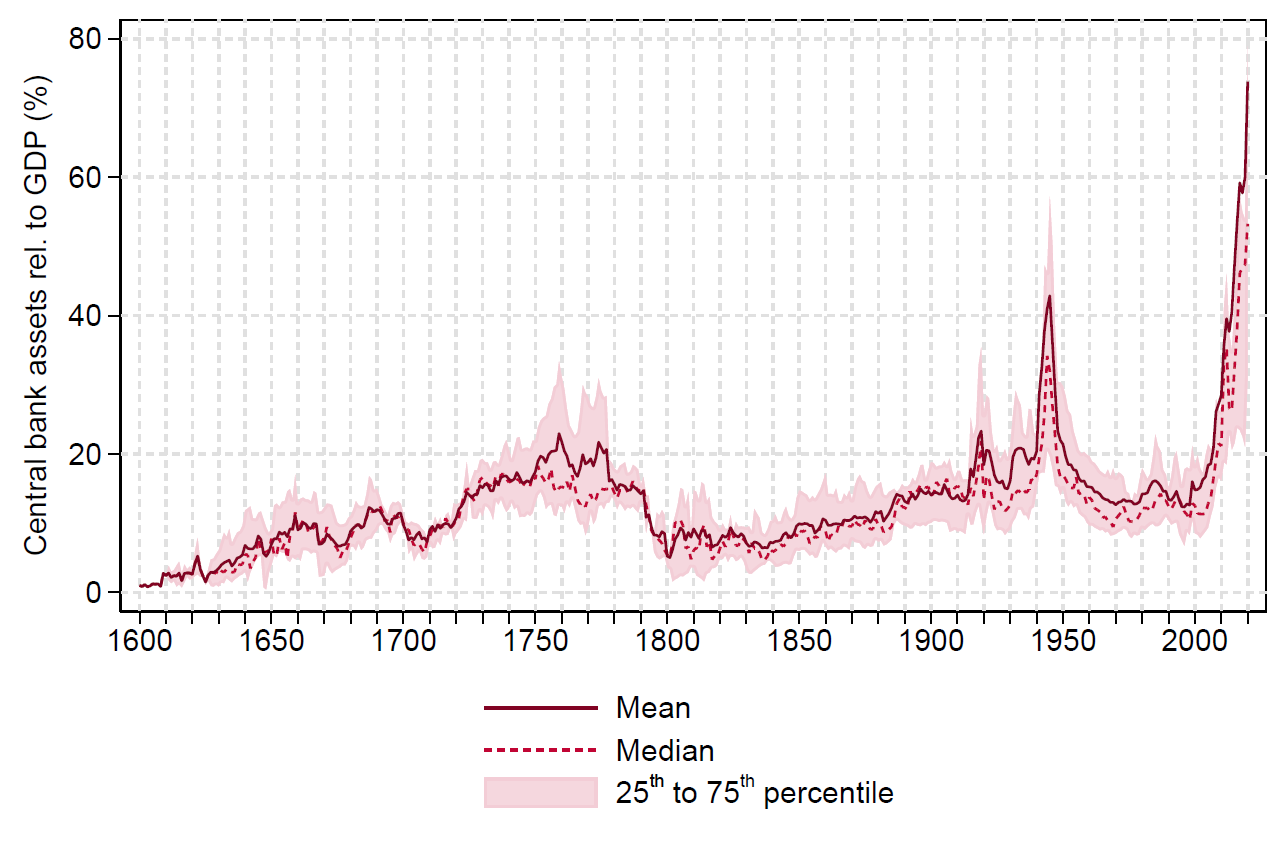

The Safety Net: Central Bank Balance Sheets and Financial Crises

with Niall Ferguson, Paul Schmelzing and Moritz Schularick

This paper studies the evolution of central bank balance sheets over the past 400 years across 17 major economies. The size of central bank balance sheets has varied substantially over time relative to economic and financial activity. Major balance sheet expansions were initially associated with government finance in geopolitical emergencies, but over time liquidity provision during financial turmoil has become the key driver of balance sheet operations. We examine the historical record of such lender of last resort interventions with a novel identification strategy based on pre-determined ideological beliefs of acting central bank governors (“hawks” vs. “doves”) with respect to financial sector support. Using exogenous variation in the crisis response, we estimate the effects of lender of last resort operations on the economy. History shows that liquidity support during financial crises has indeed tended to stabilize the economy successfully: crises are less severe, asset prices recover more quickly, and deflation is avoided. However, there is also evidence that the provision of central bank liquidity to financial markets raises the probability of future boom-bust episodes, pointing to potential moral hazard effects of central bank intervention.

Revise and Resubmit at Journal of Political Economy

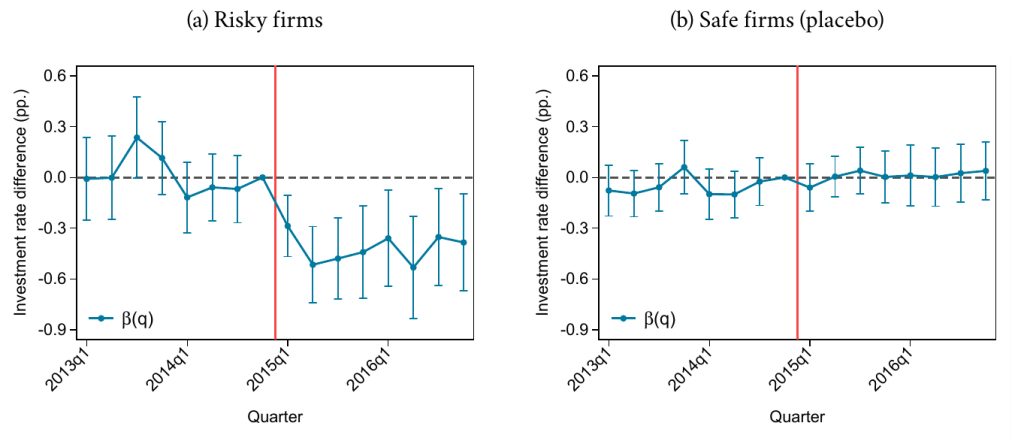

Market Creditor Protection, Finance and Investment

In contrast to traditional bank lending, bond market debt disperses the creditor base. Legal protections of dispersed market creditors can exacerbate coordination frictions and raise the cost of default. I show that market creditor protection can thus be excessive, discourage market-based lending and reduce firm investment in theory. I estimate the effects of a US court ruling which protected bond market creditors from coercive exchange offers: The ruling forced distressed firms to restructure bond market debt more frequently in costly court procedures. Healthy firms responded by cutting bond issuance and investment. Direction and magnitude of reactions indicate that over-protecting dispersed creditors can undermine public credit markets, with adverse real effects.

Work in Progress (selected)

Credit Cycles and Creditor Rights

with Shohini Kundu and Karsten Müller

Do creditor rights amplify or mitigate the macroeconomic consequences of credit cycles? Using a panel of 39 countries from 1978 to 2019, we show that credit expansions in economies with strong creditor protection are followed by smaller output losses, fewer non-performing loans, and a greater reallocation of credit away from risky borrowers. Firm-level evidence from Delaware’s adoption of antirecharacterization laws right after the Dotcom boom shows that well-protected creditors cut credit to firms with poor growth prospects, while easing credit constraints for productive firms. We rationalize our findings with a model in which strong creditor rights facilitate efficient reallocation of capital after credit booms.

Private Firms, Public Firms and Wealth Concentration

with Moritz May

We link the cost of capital of private and public firms to household wealth allocation. We document tight co-movement between US private firms’ share in aggregate business value and US household sector wealth allocated to private businesses. US household sector wealth allocated to private businesses is driven by rich households who (i) own a large share of total household wealth while (ii) allocating disproportionate shares of their portfolio to private businesses. We quantify the role of household wealth concentration for firms’ listing decision using a calibrated general equilibrium model of heterogeneous firms and households. Counterfactual analysis attributes 70% of the decline in US public firms between the 1990s and 2010s to rising household wealth concentration. Our model also highlights how inefficient public capital market institutions can reduce welfare by curtailing households’ access to liquid saving opportunities.

ON OTHER Topics

Publications

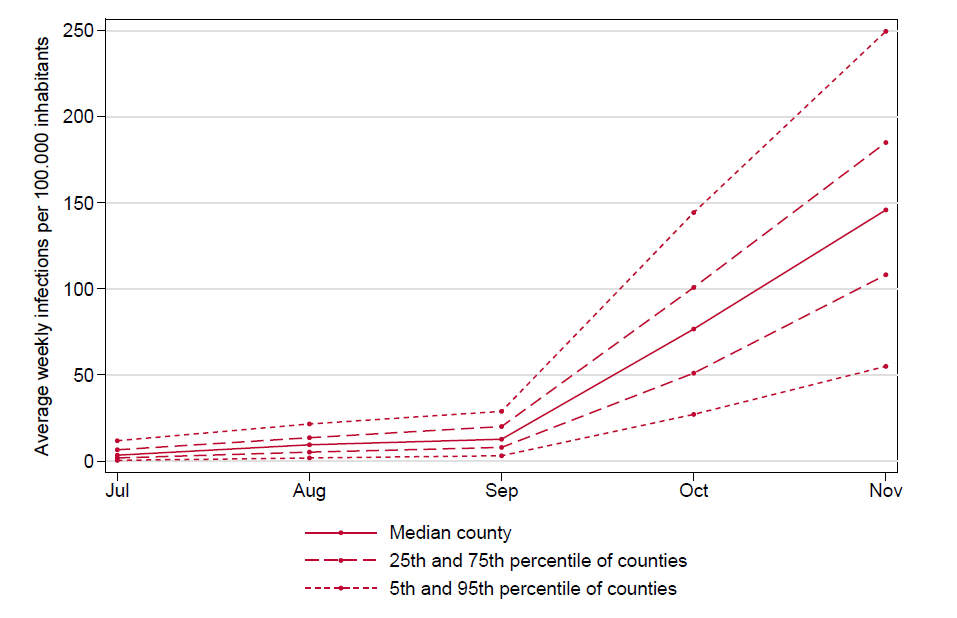

Pandemic Consumption

with Rüdiger Bachmann and Christian Bayer

This paper examines how households adjusted their consumption behavior in response to COVID-19 infection risk during the early phase of the pandemic. We use a monthly consumption survey specifically designed by the German Statistical Office covering the second wave of COVID-19 infections from September to November 2020. Households reduced their consumption expenditures on durables and social activities by, respectively, 24 percent and 36 percent in response to one hundred extra infections per one hundred thousand inhabitants per week. The effect was concentrated among the elderly, whose mortality risk from COVID-19 infection was arguably the highest.

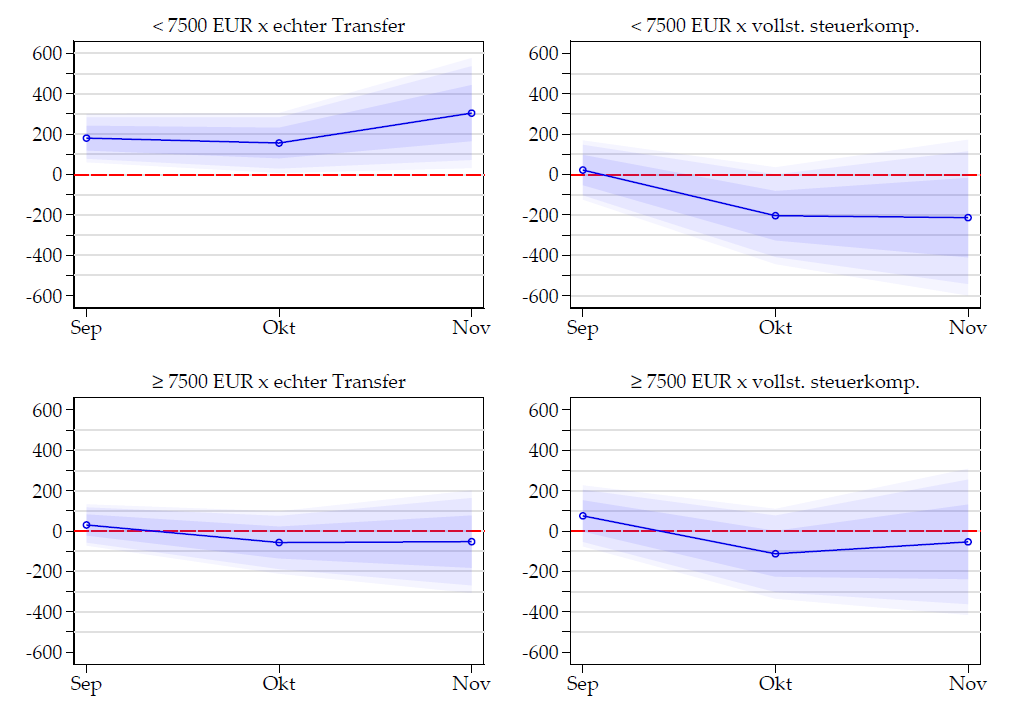

Kinderbonuskonsum

with Rüdiger Bachmann and Christian Bayer

To fight the pandemic recession of 2020 and alleviate socio-economic repercussions, the German government targeted transfers at families. We evaluate the policy’s consumption multiplier at the micro-level using representative data from a survey designed for that purpose. We document heterogeneity across families with different economic characteristics. The aggregate consumption multiplier might have been as large as 30% cumulated over three months. Our estimates cast doubt upon the reliability of households‘ self-reported consumption impulses, pointing to mental accounting biases. (Article in German)

Working Papers

Work in progress

Monetary Policy, House Prices and Regional Discount Rates

with Francisco Amaral, Steffen Zetzmann and Jonas Zdrzalek

This paper investigates the heterogeneous impact of monetary policy on house prices across geographical regions. We document substantial spatial heterogeneity in the sensitivity of house prices to monetary policy shocks. In large superstar agglomerations with low rental yields, prices decline (rise) more strongly in response to contractionary (expansionary) monetary policy compared to peripheral regions with high rental yields. We propose a mechanism based on pre-existing differences in regional discount rates for real estate assets.